ComDeCo: Composable Derivative Contracts

Project Topic

A novel component-oriented approach based on the concept of active documents for the composition and pricing of derivatives contracts

Project Description

Since their invention several centuries ago, the importance of options and derivatives has grown immensely, albeit sometimes disrupted by events like the famous tulip crisis in the 17th century. The ancestors of options and derivatives traded presently were introduced in the seventies of the last century. Due to the pressure of innovation, shortened time to market periods and a tremendously high degree of flexibility concerning the design of derivative contracts, new techniques for contract composition, contract valuation etc. have to be developed to cope with the still increasing demand for all new financial products.

ComDeCo explores new possibilities of contract composition and valuation by adapting well-known principles of component-oriented software design to the domain of financial contracts in conjunction with the development of new techniques that allow for semantic checking of user-defined contracts or modular fair price calculations, for example.

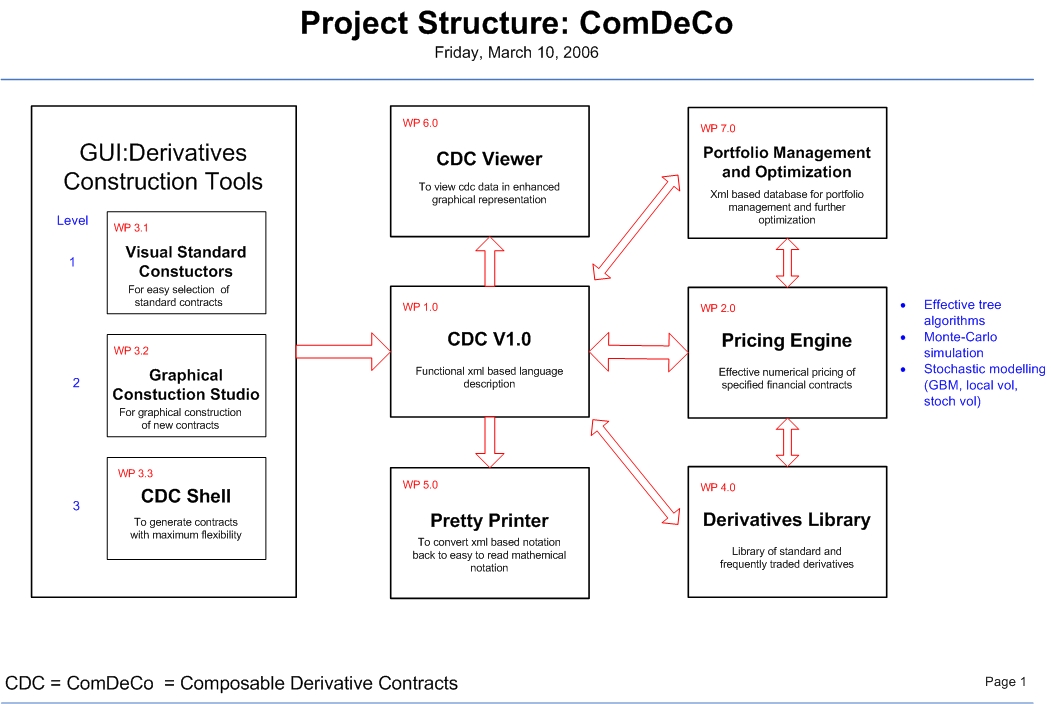

Project Structure

Project Members

Project Chair

Participating Research Groups

- Financial Mathematics and Stochastic Controlling Group (Department of Mathematics)

- Software Technology Group (Department of Computer Science)

- Sect. Financial Mathematics (Fraunhofer Institute for Industrial Mathematics (ITWM))

Scientific Personnel

- Stefanie Müller (Department of Mathematics)

- Dr. Ulrich Nögel (Sect. Financial Mathematics)

- Dipl.-Inform. Markus Reitz (Software Technology Group)

External Cooperation

- Dr. Ömür Ugur (METU Ankara)

Project Events and Achievements

Project start: 01.10.2005 with a preliminary duration until the end of 2007

Project Milestones

- 5 Mar 2006

- Initial prototypical version of ComDeCo's derivative design editor

- 15 Feb 2006

- Minimal prototype (proof of concept) demonstrating the applicability of the general-purpose Active Document framework to the domain of derivative contract modeling.

- 01 Dec 2005

- Initial specification of ComDeCo's XML-based description language

Project Publications

Thomas Gerstner, Markus Holtz, Ralf Korn. In: J. Miller, D. Edelman, J. Appleby ed.,

Numerical Methods for Finance. CRC Press, 2007

Markus Reitz, Ulrich Nögel. In:

WSEAS Transactions on Information Science and Applications. Volume 9, Number 3, P. 1756--1764, September, 2006

Markus Reitz, Ulrich Nögel. In:

Proceedings of the 7th WSEAS Int. Conference on COMPUTERS AND MATHEMATICS IN BUSINESS AND ECONOMICS (MCBE06), Cavtat, Croatia. June, 2006

Markus Reitz. In:

Proceedings of the ECOOP Workshop of Component-Oriented Programming (WCOP 06). 2006

Markus Reitz. In:

Poster Session at the European Conference on Object-Oriented Programming (ECOOP 2006). 2006

Ralf Korn, L. C. G. Rogers. In:

Journal of Derivatives. Volume 13, Number 2, P. 44--49, 2005